Protecting Your Wealth From Taxes

Tax (Photo credit: 401(K) 2012)

It's now time to face the facts. Taxes are going up.

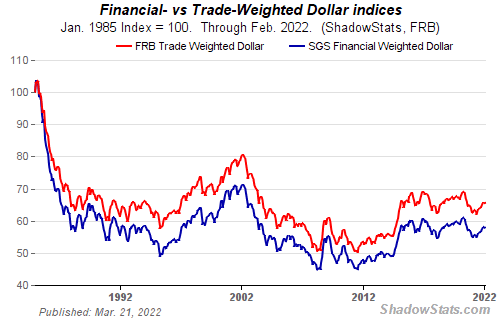

Printing money by the Fed and other central banks around the world is likely to continue for some time as a sneaky way to devalue the currency and reduce the debt burden. We see this reflected in the price of gold and silver lately and the long-term decline in the value of the dollar (chart below). This alone with not be enough, however, and taxes will need to be increased to deal with ballooning government deficits.

Nationally, the fiscal cliff is approaching, and as seen in California (a state with a long history of anti-tax sentiment), voters will allow new taxes with the right amount of special interest advertising dollars backing it. In the case of Proposition 30, taxes are being raised on "wealthy" individuals and through the sales tax to fund schools. Sorry, but if you live on a coastal city like Los Angeles or New York and you have a few kids, a mortgage, a couple of car payments and make $250K+ a year (combined) that's just not wealthy. That's middle class. Maybe in Omaha, but not in LA.

Something I wasn't aware of is that the income tax increase component of Proposition 30 is retroactive to the beginning of 2012! Where that money actually goes is anyone's guess (they say it will be used for education, but how much of it gets to the classroom is questionable). Clearly, this is a disturbing precedent. California's revolt against taxes began in 1978 with Proposition 13, which limited the rate at which property taxes could be assessed and also limited the ability to increase taxes in the future by requiring a 2/3 majority vote of legislatures or the people (if a voter initiative). 34 years later, could we be at another turning point in how the majority of voters view taxes?

Our national debt is now over $16 trillion and growing every day (check the link to the national debt clock). State budgets are bloated and state tax revenues are in decline from the after effects of the Great Recession and continued high unemployment (see chart below).

With Obamacare, taxes have already increased, including a major expansion of the Medicare tax to include net investment income (see my past blog post on this topic for more information). With Obama winning four more years, it seems likely that this trend will continue at the national level.

Clearly, if you work for a salary you will pay the price in higher taxes. Now more than ever it will be critical to make tax planning an important part of your investment and retirement planning.

Important investment tools available for anyone to use in tax planning include:

Federal (and state in some cases) tax free municipal bonds, including land secured bonds

Oil and gas master limited partnerships

Precious metals (to protect against the decline of the dollar)

Investment real property (think of it as a long term inflation protected bond - as long as the cash flow is positive)

Don't wait until it's too late. Start your tax planning now - talk to a CPA or tax preparer who is knowledgeable about your particular situation.

Related articles