Buying or Leasing a New Car

If you are thinking about buying a car, there are several things you need to know about the finances before you do. This post should help give you some insight from my experience over the years in buying cars.

1) Cash is Not King. Contrary to popular belief, assuming you have the cash available, it's not necessarily always cheaper to buy a car for cash from a dealer. They actually want you to use their financing and many times are more willing to give you a lower price or other incentives if you do so.

2) Information is Power. There are plenty of online sources to check pricing these days to avoid getting ripped off, unlike the "old days" of car buying when you were at a disadvantage trying to figure out whether you are getting a good deal or not (staring at the discount off the "sticker price"). I like Kelley Blue Book or Truecar.

3) Timing is Key. Timing is everything when buying a car. The best time to buy a car is usually around the end of the month and also after the next year's models have come out (which makes the prior year models less desirable and often with incentives in order to sell them). The best time to buy a car is probably late December since many companies' accounting years end in December and they are highly motivated to get the sales recorded.

4) Use Depreciation to Your Advantage. I like to buy previously owned cars, since they are often like new (only a few years old with low mileage) and they cost significantly less than buying a new car, saving you a lot of money. Most new cars depreciate in value rapidly and buying a used car leverages this fact to your advantage. This is particularly true if you are in the market for an electric vehicle.

5) Understand the Numbers. In my experience, I have found the best thing to do is finance the car with the dealer and then pay the loan off right away if you are planning to own the car for several years. Paying the loan off quickly can also improve your credit score. Also, many people don't understand the interest rate that is charged on the car loan and other loan terms. If you have good credit and the car dealer is anxious to sell you the car, they can often offer very low annual percentage rates as low as 1% to 4%. How are they able to do this? Well, first of all many auto manufacturers own their own finance companies and they provide low-cost financing to support their dealer network and ultimately sales. Since you have to make a substantial down payment and the loan is secured by the car, and most importantly you have good credit, there's not as much risk taken by the financing company to make a loan with that interest rate. After all, it's designed to entice you into buying the car since it makes the payment more affordable.

Also, many times finance companies / dealers will try to make the monthly payment even more affordable by stretching the repayment term out from 3 to 5 years or even longer. If your plan is to pay off the loan quickly, the interest rate and the term don't matter as much and that might help you get a lower price or other incentives on the car. Just make sure that the initial payment (until you pay off the car loan) doesn't break your budget if you do go with a higher rate and shorter loan term.

Leasing a car can also make sense for you, depending on your situation. The best thing about leasing is that you don't have to bring much cash upfront to get the car (usually less than the down payment that would be required on a loan, for example) and the monthly payment can be lower. The downside of a lease is that your payment assumes a certain amount of annual miles you drive and if you have "overage" when you return the car, you have to pay for that. You also get charged for any damage or excessive wear and tear on the car when you return it. Oftentimes, the dealer will use that "return bill" as a bargaining chip to get you to lease a new car from them at the end of your current lease, which is another potential downside. If you like getting a new car every three years or so and don't mind having a car payment all the time, then leasing might be best for you, as long as you don't lease in order to get a vehicle that you can't afford to buy outright and so long as you understand the financial impact of leasing versus buying (more on that below). Also, if you are self-employed, leasing a car for your business might make sense as a business tax deduction, but always check with your CPA first.

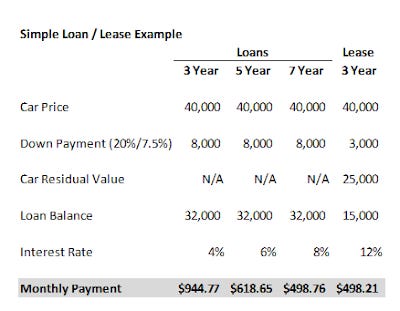

Here's how the numbers look (see table below with a simple example). You'll see that you actually pay a much higher interest rate on a lease, but the monthly payment is lower because you give back the low-mileage car at the end of the lease - the residual value of the vehicle effectively reduces the amount you are financing. Note the lower loan balance that's assumed ($40,000 car price less $25,000 residual value equals "loan" amount of $15,000). Typically the lease includes a rent charge in addition to the vehicle depreciation, but for simplicity I have combined the two into one amount of $15,000 for this example. The down payment of $3,000 is really just a prepayment of the lease and can be any convenient amount the dealer wants to charge. This is frequently discounted in order to entice you into leasing the car, depending on how motivated the dealer is to move the car off their lot.

A few take-aways on loans: Longer loan terms can carry higher interest rates, but overall you get a lower monthly payment since you have more time to pay the loan off. Down payments can also vary depending on the situation, but for simplicity I just assumed 20% below except for the lease situation described previously. Also, it's important to note that this example does not include taxes, title, registration, license, dealer fees and other up-front payments required when buying a car. It's also important to remember that most likely your insurance will go up when buying a new car and that needs to be budgeted as well.

As you can see, the highest monthly payment is for a 3 year loan and the lowest monthly payment is for a 3 year lease. Even with the 3 year loan at 4%, you will still pay over $2,000 in interest over the life of the loan, which is why paying off early is always a good idea if you can do it. Sometimes you can pay off in "chunks" like when you get your annual bonus or when you get your tax refund. Also, in the lease example, you will pay almost $3,000 in interest over the life of the lease (50% more than the loan example). This is significant and not well understood by consumers, since both the car buyer and the dealer focus only on the monthly payment and not on the "cost of money." Unlike a loan, you cannot prepay a lease, although you may be able to "buy out" of it before the end of the term for a fee or possibly the dealer may let you out if you lease a new vehicle. That's also important to consider when deciding whether to lease or buy.

I hope you find this post useful as you chart your personal financial course and Build a Financial Fortress this year.

To see all my books on investing and leadership, click here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.