Bitcoin vs Compounding Debt

When the Numbers Outgrow the System

Compounding is neutral.

It does not care whether it applies to savings or to debt.

It does not respond to political preference.

It operates according to arithmetic.

When applied to capital, compounding builds wealth.

When applied to obligations, compounding builds pressure.

For a long time, many governments were able to grow debt while keeping the cost manageable. After the Global Financial Crisis — and especially through the ultra-low rate era of the 2010s — debt rose, but interest rates fell. The burden felt contained.

That regime changed.

The Global Scale of the Problem

According to the International Monetary Fund, total global debt has stabilized at elevated levels — above 235% of global GDP — with public debt near 93% of global GDP, representing roughly $99 trillion in sovereign obligations.

Public debt alone is now projected to exceed 100% of global GDP later this decade.

The scale is historic.

But the scale is not the mechanism.

The mechanism is cost.

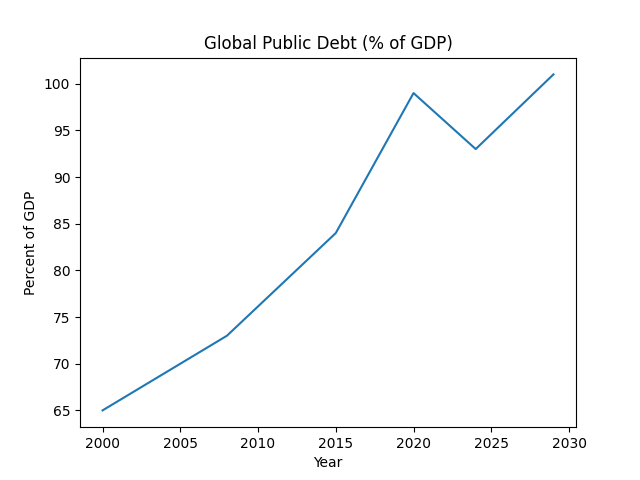

📊 Chart 1 — Global Public Debt (% of GDP)

Global public debt has risen materially since 2000 and is projected to exceed 100% of GDP later this decade (IMF).

Debt is a stock.

Interest is a flow.

When interest rates are low, large debt stocks feel manageable.

When rates rise, the cost of servicing existing obligations expands quickly.

At modest debt levels, higher rates are inconvenient.

At high debt levels, they become structural.

This is not a U.S.-only story.

Japan, the euro area, the United Kingdom, and the United States operate in different institutional contexts. But the arithmetic of interest expense behaves the same everywhere.

Large sovereign balance sheets built in a low-rate world must now function in a higher-rate one.

Sovereign Debt Is Not “Too Big” — Until It Becomes Too Sensitive

Debt is often framed morally — prudent versus reckless.

A more useful framing is sensitivity.

How sensitive is the budget to interest rates?

How quickly does the interest bill grow as debt rolls over?

How much fiscal room remains when interest becomes a top-tier expenditure?

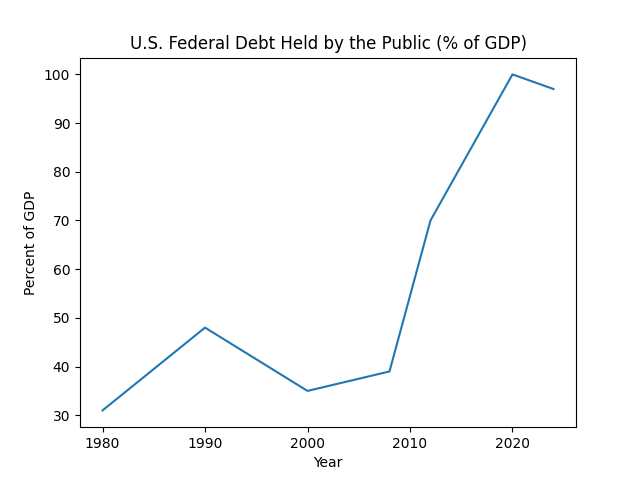

In the United States, federal debt held by the public has risen sharply since 2008 and surged again after 2020.

📊 Chart 2 — U.S. Federal Debt Held by the Public (% of GDP)

U.S. public debt has expanded sharply since 2008, with step changes following major crises (CBO historical data).

When debt reaches scale, refinancing risk becomes constant. Governments must continuously roll over maturing obligations. Each rollover occurs at prevailing market rates.

If rates are higher than when the debt was issued, the cost rises.

This is where compounding turns visible.

Interest Expense Changes the System

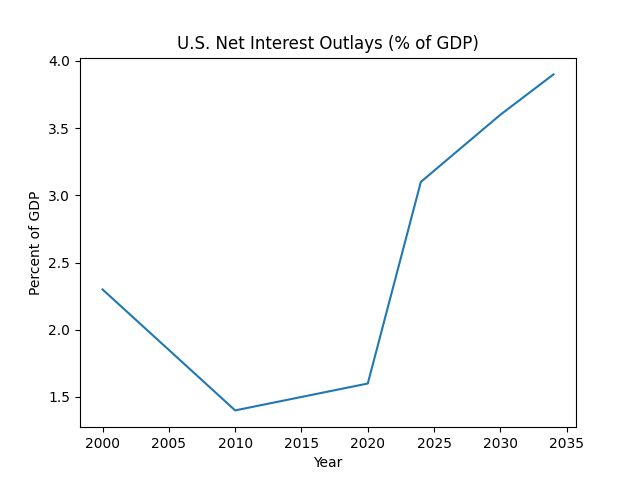

The Congressional Budget Office projects that U.S. net interest outlays will rise toward 3.9% of GDP by 2034, approaching levels historically associated with major fiscal inflection points.

Interest is not a discretionary line item.

It is contractual.

Every dollar spent on interest is a dollar not spent elsewhere. And unlike most budget categories, it cannot be cut without restructuring obligations.

📊 Chart 3 — U.S. Net Interest Outlays (% of GDP)

Rising interest outlays illustrate how compounding obligations increase fiscal sensitivity (CBO projections).

When debt is modest, tightening corrects excess.

When debt is large, tightening exposes dependence.

If central banks raise rates aggressively, the cost of financing sovereign debt rises. If fiscal authorities attempt rapid consolidation, growth may slow, reducing tax revenue and widening deficits. If markets perceive instability, borrowing costs can rise further, amplifying the cycle.

Discipline, which is meant to restore balance, begins to introduce fragility.

This is the trap.

The Trap: When Discipline Becomes Destabilizing

At high debt levels, interest expense is no longer marginal. It is material. Each percentage point increase in rates meaningfully increases the cost of servicing existing obligations.

As maturing debt rolls over at higher yields, the interest bill compounds.

The arithmetic accelerates.

What was once a policy lever becomes a structural pressure point.

The longer large debt stocks persist, the more the system adapts to accommodation. Financial institutions structure portfolios around prevailing rates. Governments budget assuming manageable financing costs. Asset prices reflect liquidity conditions.

Accommodation becomes embedded.

Removing it becomes disruptive.

Reducing debt requires surplus and restraint.

Managing debt requires stability and liquidity.

Once management replaces reduction as the primary objective, the bias tilts toward accommodation.

Not because policymakers lack discipline.

But because the arithmetic narrows their choices.

Debt compounds.

Interest compounds.

Sensitivity compounds.

Bitcoin and the Absence of Compounding Obligations

Sovereign debt carries embedded claims on future output.

Bitcoin carries none.

Bitcoin does not represent a liability of any government. It does not embed an interest obligation. It does not require refinancing. It does not depend on rollover markets or yield curves.

It does not compound in the way debt compounds.

Its issuance schedule is fixed and known. It does not expand to ease fiscal strain. It cannot be diluted to lower interest burdens. It does not depend on policy credibility to maintain its supply.

It does not require growth to remain solvent.

In a high-debt world, that distinction matters.

Sovereign systems must manage liabilities.

Bitcoin has none.

Sovereign currencies must balance stability with refinancing risk.

Bitcoin carries no rollover risk.

As sovereign sensitivity increases, Bitcoin’s monetary base remains unchanged.

It simply continues to produce blocks.

Conclusion

Compounding is neutral.

It builds wealth when applied to savings.

It builds pressure when applied to obligations.

For decades, sovereign systems benefited from falling rates that masked rising debt.

In a higher-rate world, the arithmetic is more exposed.

Political cycles strain money.

Demographic cycles strain it further.

Compounding debt narrows the corridor.

When obligations become large enough, discipline itself becomes destabilizing.

Debt compounds.

Interest compounds.

Sensitivity compounds.

Bitcoin does not.

Arithmetic does not negotiate.

Bitcoin does not either.

Not financial or legal advice, for entertainment only, do your own homework. I hope you find this post useful as you chart your personal financial course and Build a Bitcoin Fortress in 2026.

Thanks for following my work. Always remember: freedom, health and positivity!

Please also check out my Bitcoin Fortress Podcast on all your favorite streaming platforms. I do a weekly Top Bitcoin News update every week on Sunday, focused on current items of interest to the Bitcoin community. Please check it out if you haven’t already. Also now on Fountain, where you can earn Bitcoin just for listening to your favorite podcasts.

Also, check out my books:

Follow me on Nostr:

npub122fpu8lwu2eu2zfmrymcfed9tfgeray5quj78jm6zavj78phnqdsu3v4h5

If you’re looking for more great Bitcoin signal, check out friend of the show Pleb Underground here.

Kind of see the end of unstoppable fiat money printing, bond issuing, compunding interest ... that will inevitably cause stagflation in the S/M term. And if you add in billions spent on a daily basis to finance totally useles wars, the end of fiat is getting closer and closer worldwide. BITCOIN fixes that because it doesn't have a CEO, is not controlled by politics, WS and most of all Bitcoin is not and never will be printed out of thin air. 21M units. That's it. Period.