Are We Starting to See the "Aftershock" of the Great Recession?

It's been a while since I read "Aftershock" by David and Robert Wiedemer and Cindy Spitzer, which I have included in my recommended reading list. In the book, originally published in 2011, the authors lay out the case for what lies ahead as the dollar bubble and government debt bubble begin to burst (the last two bubbles in our so-called "bubble economy"). Could this be unfolding now with the recent stock market sell-off?

When these bubbles burst, the authors claim that there are only two asset classes that you should be invested in: cash and gold - mostly gold. All other asset classes, including stocks, bonds, real estate, whole life insurance policies, etc. will suffer significant declines in value.

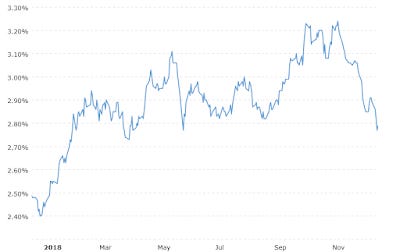

There may well be very good values in these non-cash/gold asset classes at some point in the future, but only after the bubbles have burst. At the core of their concern is the Federal Reserve printing money (lowering interest rates / quantitative easing) to stimulate the economy - they believe this is highly inflationary and that in the next one to three years, we could see very high rates of inflation - perhaps as much as 10% per year. They might have been a little too early with this call, but not completely off the mark. Indeed, despite the Fed raising short term interest rates recently, the bond market already sensed growing inflation, which is why longer term interest rates have been climbing rapidly over the past year, as shown in the 10-year Treasury chart below:

10-Year Treasury Rate - One Year (courtesy of www.macrotrends.net)The recent drop in Treasury rates is likely more due to uncertainty and a flight to safety from stock market losses, rather than a change in inflation expectations.

I was a little surprised to see real estate included in the "avoid" category. I have long believed that investment property, especially residential real estate, that provides positive cash flow would weather an inflationary storm pretty well. We would normally expect the value of the asset to increase with inflation and your equity should further increase as the mortgage is paid down. Also, the largest cash outflow (the mortgage payment) is fixed, while rental income and other expenses should increase at about the same rate as inflation, which means your cash flow should grow faster over time. Of course in a recession, you could face falling rents in order to maintain occupancy. In that case you could potentially see negative cash flow, especially if you recently purchased the property. If the negative cash flow is sustained and you can't support it, you could be forced to sell the property at a loss.

The recent sell-off in the stock market adds to the credibility of their argument that there has been no real economic recovery since the Great Recession and the stock market increase can be largely attributed to the money printing operations of the Federal Reserve (which include keeping interest rates very low and quantitative easing, or purchasing of bonds in the open market to artificially lower interest rates). This is especially true if you believe that official statistics such as inflation and unemployment are under-reported due to changes in how the measures are calculated over the years.

In addition to the low interest rates, the government has also applied fiscal stimulus in the form of tax cuts and spending increases, further inflating the government debt bubble which was already growing with persistent deficits. Higher interest rates and debt balances also increases the amount of interest the government has to pay on all that debt, which further increases borrowings to cover the payments. As the Aftershock authors correctly point out, the cure will become the poison in the form of inflation and ultimately destabilization of markets due to over-leveraging.

Ironically, the "safe haven" investment of choice is US government debt each time the stock market sells-off, but that may soon change to gold (and to a lesser extent the other precious metals) when inflation becomes more significant.

If you haven't read this book, I'd recommend it. I'd also recommend you look at your portfolio and consider changing your strategy to adjust to these economic times. Check out my recent blog post on the subject here.

For more investing ideas, click here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.